Knowing why high-risk payment approvals get delayed can save online merchants a great deal of time, friction, and avoidable back-and-forth during the application process. For many businesses, delays do not happen because the company is automatically a bad fit. They happen because the underwriter sees unanswered questions, incomplete context, or operational signals that suggest more risk than the merchant may realize.

That is what makes underwriting so important in high-risk payments. Approval is not based on one form, one website, or one sales pitch. It depends on how clearly the business presents its model, its transaction patterns, its customer journey, and its ability to manage disputes, refunds, and compliance expectations. If any of those areas look unclear, approval timelines tend to stretch.

For online merchants, understanding why high-risk payment approvals get delayed is not just useful before applying. It is one of the most practical ways to improve approval odds, reduce friction, and enter the process with realistic expectations.

What underwriting is really evaluating

To understand why high-risk payment approvals get delayed, it helps to first understand what underwriting is designed to do.

Underwriting is not simply checking whether a business exists. It is a risk review process. Payment providers want to know whether a merchant is likely to process legitimate transactions, deliver what it promises, manage customer complaints properly, and keep fraud and chargebacks under control. They also want to know whether the merchant’s business model aligns with the traffic, offers, billing structure, and jurisdictions involved.

In other words, the underwriter is not only assessing the product. They are assessing the entire commercial operation behind it.

This is why businesses with genuine revenue and real demand can still face delays. The issue is often not the business itself. The issue is that the provider does not yet have enough confidence in how that business operates.

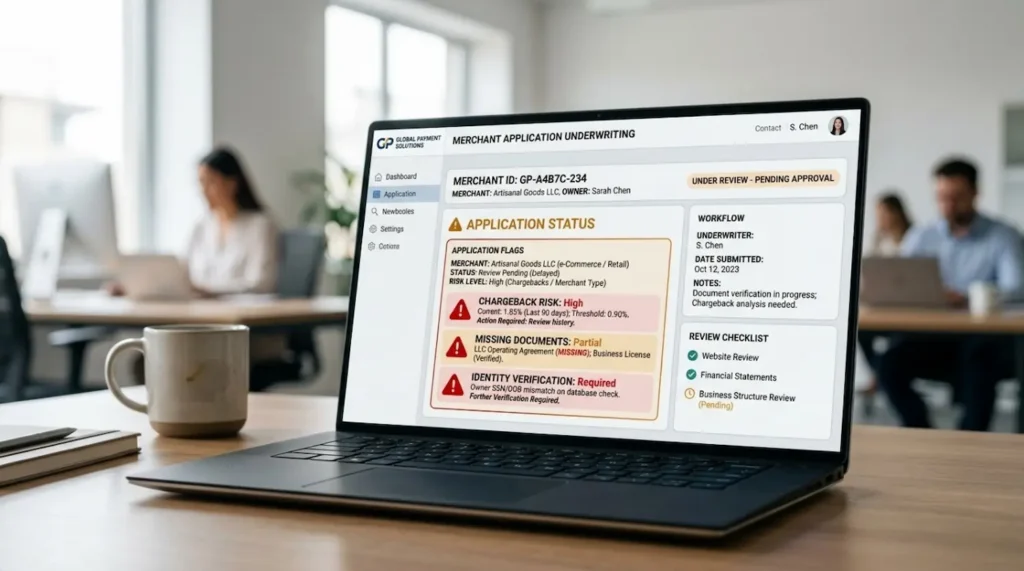

Incomplete or inconsistent business documentation

One of the most common reasons why high-risk payment approvals get delayed is incomplete or inconsistent documentation.

This sounds simple, but it remains one of the biggest causes of friction. A merchant may submit company registration documents, bank statements, proof of address, processing history, or beneficial ownership information, yet one small mismatch can slow everything down. A business name formatted differently across documents, a missing director record, an outdated address, or unclear ownership structure can trigger extra review.

From the provider’s perspective, these are not minor details. They are early trust signals. If core business information is fragmented or inconsistent at the start, the underwriter may assume other areas of the operation will require closer scrutiny too.

This is one reason merchants benefit from following a structured onboarding checklist before they submit anything. When documents are prepared in advance and aligned properly, the review process becomes much smoother and far less reactive.

A website that creates more questions than answers

Another major factor behind why high-risk payment approvals get delayed is the website itself.

Many merchants underestimate how heavily a payment provider will rely on website review during underwriting. The site is often the first place an underwriter checks to understand what the business sells, how billing works, what the customer experience looks like, and whether the operation appears transparent and credible.

Problems often appear when the website has vague product pages, missing legal pages, weak refund language, broken links, misleading claims, or checkout flows that do not match the business description in the application. If the provider sees a disconnect between the merchant’s stated business model and the actual customer-facing experience, approval can quickly slow down.

For example, if a merchant claims to sell supplements but the site copy, fulfilment language, or billing flow resembles a subscription or continuity model, the provider may need more clarification. The same applies when product descriptions are too thin, shipping details are missing, or the site does not clearly explain recurring billing terms.

In high-risk underwriting, clarity matters. A clean and transparent site does not guarantee approval, but a confusing one is one of the clearest answers to why high-risk payment approvals get delayed.

Unclear processing history or unrealistic projections

A payment provider also wants to understand how the business has processed payments in the past and what it expects to process in the future.

If a merchant has no prior history, that does not automatically prevent approval, but it does increase uncertainty. If the business does have prior history but provides incomplete statements, inconsistent volumes, or unrealistic future forecasts, the underwriter may pause to reassess the risk.

This is especially common when online merchants project large monthly volumes without enough operational proof behind them. Ambitious growth is not a problem in itself, but if the numbers look disconnected from the business’s current stage, traffic profile, or fulfilment capability, delays become more likely.

This is another practical reason why high-risk payment approvals get delayed. Underwriters want confidence that transaction volume, average ticket size, refund exposure, and customer acquisition patterns all make sense together. If those pieces do not align, the file often moves into deeper review.

Chargeback exposure remains one of the biggest red flags

If there is one issue that consistently shapes why high-risk payment approvals get delayed, it is chargeback exposure.

From the provider’s perspective, chargebacks signal more than just customer dissatisfaction. They can point to poor fulfilment, unclear billing, weak support, misleading advertising, fraud vulnerability, or unstable customer expectations. In high-risk sectors, even a modest pattern of disputes can make an underwriter much more cautious.

This matters even more for businesses in industries where disputes already tend to run higher. Subscription models, nutraceuticals, adult, coaching, digital goods, dating, and certain cross-border offers are all reviewed more closely because the provider knows that customer complaints can escalate quickly when expectations are not managed well.

That is why merchants should not treat dispute prevention as something to solve after approval. If a business already shows signs of exposure, the provider may delay the application while reviewing the merchant’s policies, support flow, descriptors, billing logic, and refund handling. A stronger strategy for reducing chargebacks in high-risk industries can directly improve how the business is perceived during underwriting.

Business model complexity can slow down the review

Not all high-risk businesses are delayed for the same reason. Sometimes the issue is simply complexity.

A merchant may operate across several countries, sell through multiple traffic sources, combine one-time and recurring billing, use affiliate-driven acquisition, or run an offer that changes depending on customer segment. None of that automatically makes the business unacceptable, but it can make it harder for an underwriter to form a fast and confident assessment.

This is particularly relevant for merchants with layered models such as lead generation plus fulfilment, subscription plus upsells, or a hybrid business that combines digital access with physical products. The more moving parts involved, the greater the need for explanation and documentation.

In these cases, why high-risk payment approvals get delayed often comes down to the provider needing a fuller picture. They want to know exactly how the sale happens, when the customer is charged, when fulfilment occurs, what happens in the event of cancellation, and where disputes are most likely to arise.

A business with a complex model can still be approved successfully, but only when that complexity is explained clearly rather than left for the underwriter to interpret alone.

Reserve expectations and financial risk controls

Merchants often focus on approval itself, but providers are also evaluating what protections they may need after approval. This is another reason why high-risk payment approvals get delayed.

If the business operates in a category with delayed fulfilment, elevated refund risk, or volatile customer behavior, the provider may consider financial safeguards before moving forward. One of the most common examples is rolling reserves, which help offset potential losses by holding back a percentage of processed funds for a defined period.

From the merchant side, this can feel like an unexpected complication. From the provider side, it is part of risk management. The same applies to pricing. A high-risk business may not receive the same structure as a low-risk merchant because the provider is factoring in fraud exposure, operational risk, and dispute history when setting payment processing fees.

This does not always mean the deal is deteriorating. In many cases, it means the underwriter is trying to find terms that match the actual risk profile rather than reject the account outright. Still, when a merchant is not prepared for discussions around reserves, fees, and risk controls, the review process often becomes slower and more fragmented.

Weak compliance and fraud controls

A provider also wants evidence that the merchant is capable of operating responsibly after approval.

That includes fraud monitoring, customer verification where relevant, billing transparency, and internal controls for handling suspicious activity. If the business appears to rely on aggressive acquisition without showing how fraud and abuse will be managed, the provider may delay the application until those concerns are addressed.

This is especially true for cross-border merchants, online-first businesses, and brands in verticals already associated with elevated fraud rates. If the provider cannot see how the merchant intends to identify risky transactions, limit abuse, or deal with regulatory scrutiny, confidence drops quickly.

This becomes yet another answer to why high-risk payment approvals get delayed. The underwriter is not just reviewing whether the merchant can sell. They are reviewing whether the merchant can sell at scale without creating avoidable risk for the processor.

Why communication gaps make delays worse

Even when the merchant is fundamentally approvable, delays can grow longer if communication is slow, reactive, or incomplete.

Many businesses respond to underwriting questions one message at a time without giving the full context behind the business model, billing setup, or customer journey. This creates a stop-start approval experience where the provider has to keep requesting clarification rather than progressing the file efficiently.

Good communication matters because high-risk underwriting is rarely fully automated. It is usually a dialogue. The faster the merchant can explain how the offer works, how customers are billed, how refunds are handled, and how the operation manages disputes, the easier it becomes for the provider to make a confident decision.

That is why merchants applying for a high-risk payment gateway approval should think beyond the application form itself. The process often depends on how well the business can answer operational questions in a clear, credible, and complete way.

How online merchants can reduce approval delays

Understanding why high-risk payment approvals get delayed is most useful when it leads to practical improvements before applying.

The businesses that move through underwriting more efficiently usually do a few things well. They prepare documentation carefully. They make sure the website reflects the actual customer journey. They explain their business model clearly. They show awareness of dispute risk. They are realistic about volume, geographies, and expected terms. And they anticipate questions around reserves, fees, and compliance before the provider has to raise them.

In practical terms, that means reviewing legal pages, refund language, billing disclosure, company records, banking documents, prior processing statements, and customer support workflows before the application is submitted. It also means looking honestly at operational weak points. If the business already knows it needs stronger refund handling or better fraud controls, it is far better to address that early than to wait until underwriting identifies it first.

A smoother path to approval

For online merchants, the real lesson behind why high-risk payment approvals get delayed is that underwriting is not simply about risk labels. It is about confidence.

When a payment provider sees a business that is transparent, prepared, well-documented, and operationally coherent, approval tends to move faster. When the file contains gaps, contradictions, weak customer-facing signals, or unclear exposure to disputes and loss, delays become much more likely.

The strongest high-risk merchants are not always the ones with the biggest volumes. They are often the ones that make underwriting easier to assess, easier to trust, and easier to approve.

At NiftiPay, we work with online merchants in complex and high-risk sectors to help reduce unnecessary friction during the approval process. By aligning business models, documentation, and operational expectations earlier, it becomes much easier to move from application to live processing with fewer delays and fewer surprises.

Leave a Reply